Buying a home is the single-largest financial commitment most people ever make. And sorting through mortgages involves a lot of critical choices. One of these is choosing between a fixed or variable interest rate mortgage.

True to its name, fixed-rate mortgage interest is “fixed” throughout the life of the loan. In contrast, the interest rate on a variable-interest rate loan can change over time. The mortgage interest rate charged by a variable loan is usually based on an index, which means payments could move up or down, depending on prevailing interest rates.1

Fixed-rate mortgages have advantages and disadvantages. For example, rates and payments remain constant despite the interest rate climate. But fixed-rate loans generally have higher initial interest rates than variable-rate mortgages; the financial institution may charge more because if rates go higher, it may lose out.

If prevailing interest rates trend lower, a fixed-rate mortgage holder may choose to refinance, and that may involve closing costs, additional paperwork, and more.1

With variable-rate mortgages, the initial interest rates are often lower because the lender is able to transfer some of the risk to the borrower; if prevailing rates go higher, the interest rate on the variable mortgage may adjust upward as well. Variable-rate mortgages may allow borrowers to take advantage of falling interest rates without refinancing.1

One of the biggest advantages variable-rate mortgages offer can be one of their biggest disadvantages as well. Rates and payments are subject to change, and they can rise over the life of the loan.

Should you choose a fixed or variable mortgage? Here are four broad considerations:

First, how long do you plan to stay in the home? If you plan on living in the home a short time before selling it, you may want to consider a variable-rate mortgage. With a shorter time frame, the loan will have less time to move up or down.

Second, what’s happening with interest rates? If interest rates are below historic averages, it may make sense to consider a fixed rate. On the other hand, if interest rates are above historic averages, it may make sense to consider a variable-rate loan. Then, if interest rates decline, your interest rate may fall as well.

Third, under what conditions can the lender adjust the rate and payment? How frequently can it be adjusted? Is there a limit on how much it can be adjusted in each period? Is there a lifetime limit on how high the interest rate and payment can be raised?

And fourth, could you still afford your monthly payment if interest rates were to rise significantly? How would it affect your finances if your payment were to rise to its lifetime limit and stay there for an extended period?

For most, buying a home is a major commitment. Selecting the most appropriate mortgage may make that long-term obligation more manageable.

1. Investopedia.com, April 23, 2021

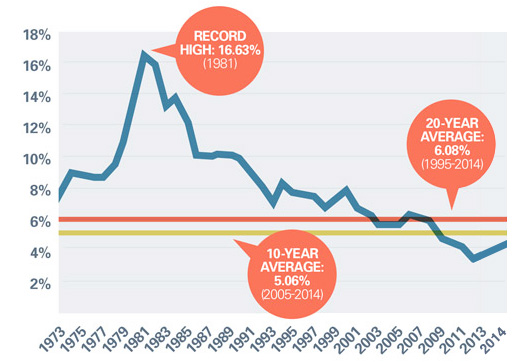

Average Interest Rate: 30-Year, FixedRate Mortgages

According to the Federal Reserve Bank of St. Louis, the average rate annually on 30-year, fixed-rate mortgages was 3.94 percent in 2019.

Source: FRED.StLouisFed.org, 2020

The content is developed from sources believed to be providing accurate information. The information in this material is not intended as tax or legal advice. It may not be used for the purpose of avoiding any federal tax penalties. Please consult legal or tax professionals for specific information regarding your individual situation. This material was developed and produced by FMG Suite to provide information on a topic that may be of interest. FMG Suite is not affiliated with the named broker-dealer, state- or SECregistered investment advisory firm. The opinions expressed and material provided are for general information, and should not be considered a solicitation for the purchase or sale of any security. Copyright 2021 FMG Suite.